Understanding insurance deductibles is crucial for anyone seeking to navigate the world of insurance effectively. Deductibles can significantly impact your financial liability, especially in times of claim. In this article, we will delve into what insurance deductibles are, how they influence your premiums, the various types of deductibles available, and tips on how to choose the right deductible for your needs. By gaining a clearer understanding of these components, you'll be better equipped to make informed decisions regarding your insurance policies.

1. What Is an Insurance Deductible?

An insurance deductible is the amount of money you are required to pay out-of-pocket before your insurance company steps in to cover the remaining costs. It is a common feature found in many insurance policies, including health, auto, and home insurance. Understanding how deductibles work is essential for managing your insurance expenses effectively.

When filing a claim, the deductible is subtracted from the total amount of the claim, meaning you will need to settle the deductible before receiving any reimbursement from the insurer. For example, if you have a $1,000 deductible and incur a loss of $5,000, you will pay the first $1,000, and your insurance will cover the remaining $4,000.

Deductibles can vary significantly from one policy to another. They can be set as a fixed dollar amount or as a percentage of the claim. Higher deductibles often mean lower premiums, while lower deductibles result in higher premiums. It’s crucial to analyze your financial situation to decide which deductible level is suitable for you.

In addition to the standard deductible, some policies also incorporate specific deductibles for different types of coverage. For example, the deductible for collision coverage may differ from that of comprehensive coverage. As such, it's important to read the fine print of your insurance policy to understand how deductibles apply in various scenarios.

- Deductibles can lower your monthly premium payments.

- They require you to pay upfront costs before insurance kicks in.

- Different policies may have different deductibles for various types of coverage.

- They can significantly influence your out-of-pocket expenses during a claim.

Overall, understanding the basic concept of an insurance deductible is the first step toward making informed decisions regarding your insurance policies and planning for unexpected costs. Being aware of how deductibles function is particularly important as you compare different insurance plans and look to find the best fit for your financial situation.

2. How Do Deductibles Affect Your Premiums?

Deductibles play a critical role in determining your insurance premiums, which are the monthly or annual payments you make to maintain your coverage. Generally, the higher your deductible, the lower your premium, and vice versa. This principle stems from the fact that when you opt for a higher deductible, you are taking on a larger portion of the financial risk associated with insurance claims. This shift in risk often results in lower costs for the insurer, leading to reduced premiums for policyholders.

- High deductible plans can save you money on daily premiums.

- A lower deductible means higher monthly premiums but less out-of-pocket expense during a claim.

- Finding a suitable balance between premiums and deductibles is crucial to ensuring affordability.

- Understanding your usage and risk factors can help you choose an appropriate deductible level.

Ultimately, recognizing how deductibles affect your premiums is essential for selecting the right insurance plan that aligns with your financial strategy. It is always recommended to evaluate your risk tolerance and consider consulting an insurance expert to ensure that you find a plan that provides the desired coverage without overextending your budget.

3. Types of Insurance Deductibles

Insurance deductibles can be categorized into various types, each serving distinct functions within different kinds of insurance policies. Understanding these types of deductibles can help you tailor your insurance choices to meet your individual needs.

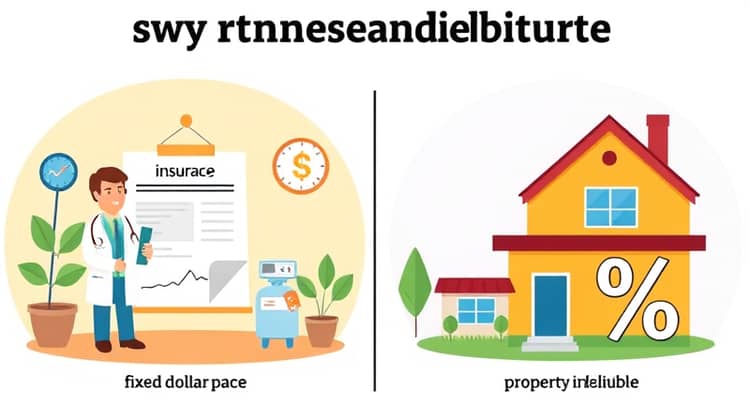

The most common type is the standard deductible, which is generally a fixed dollar amount that you pay before claims are processed. For instance, health insurance plans typically have annual deductibles that must be met before the plan pays for covered services beyond preventive care.

Another type is the percentage deductible, which is a certain percentage of the total claim amount that must be paid by the insured party. This type is frequently found in property insurance policies, where it might apply to damage assessments and losses.

Lastly, there are varying deductibles specific to certain coverages, like collision and comprehensive deductibles in auto insurance. Each type has a strategic purpose and can significantly influence your overall insurance experience.

- Standard Deductibles: A fixed amount you pay before insurance helps with claims.

- Percentage Deductibles: A designated percentage of a claim that you must cover.

- Specific Deductibles by Coverage: Different deductibles for different types of coverage, such as collision vs. comprehensive.

- Aggregate Deductibles: A total deductible for multiple claims within a specified period.

Being informed about the types of insurance deductibles allows you to make better decisions regarding your policy options. The right type can align with your financial situation and risk tolerance, ensuring that you have both adequate coverage and manageable out-of-pocket costs.

Evaluate your options carefully to choose the deductible types that work best for you and your unique circumstances. Consulting an insurance professional can also provide valuable insight into which type of deductible may suit your lifestyle and financial goals.

In summary, understanding the various types of deductibles sets the stage for informed decisions when selecting an insurance policy, ultimately leading to improved financial management in unexpected situations.

4. Choosing the Right Deductible

Selecting the right insurance deductible requires a careful assessment of your financial status, risk tolerance, and how much you can afford to pay out-of-pocket. This strategic decision can significantly impact your financial well-being during claims.

When evaluating potential deductibles, consider your typical healthcare costs, driving habits, and any specifics related to your property or assets. These elements can help determine a threshold that you can comfortably manage during unforeseen circumstances.

Additionally, weigh the potential long-term savings of a higher deductible against the upfront cost you would incur in the event of a claim. This will involve predicting the likelihood of needing to file a claim and balancing that with your financial capabilities.

- Consider your financial situation and your ability to pay deductibles upfront.

- Evaluate your lifestyle risks to determine an appropriate deductible level.

- Analyze potential savings on premiums with varying deductible amounts.

Ultimately, selecting the right deductible is about striking the right balance between your premium costs and potential out-of-pocket expenses. This decision can have lasting implications, so take the time to evaluate various options and consult with an insurance agent if needed.

As you think about your deductible options, remember there is no one-size-fits-all approach; what works for one individual may not work for another.

Evaluate your choices holistically and make sure to choose a deductible that supports both your immediate needs and long-term financial health.

Conclusion

Understanding insurance deductibles is essential for managing your insurance policies effectively. This knowledge enables you to make informed decisions that can save you both money and stress in the event of a claim.

A well-thought-out approach to selecting your deductible can help you find the right balance between paying less in premiums while still ensuring you’re adequately covered when you need it most.

In conclusion, your choice of deductible plays a pivotal role in your overall insurance strategy and can influence not only your premium payments but also your financial peace of mind during unexpected circumstances.